With a market share of 15.5%, $1.8 billion-asset Santa Cruz County Bank (SCCB) ranks fourth in California’s Santa Cruz county, trailing only megabanks. Krista Snelling, president and CEO, believes the community bank’s strong performance reflects its strategy of investing in up-to-date technology to serve and therefore strengthen customer relationships.

Snelling created SCCB’s digital transformation committee when she joined the community bank in 2021. Composed of SCCB executives, IT leaders and some client-facing team members, the committee’s mission is to identify and prioritize opportunities for technology upgrades.

The community bank started with small improvements that simply required policy changes as opposedto major technology investments. “I chipped away at things that we could do that were in our control and we could do really quickly,” Snelling recalls. “Then we started to look to the technology.”

SCCB’s tech revolution

Gradually, SCCB implemented numerous initiatives aimed at efficiency, such as teller cash recyclers, teller deposit capture and cashier check automation. “We’ve made significant investments in both client-facing and back-office technologies that create a better and safer client experience,” Snelling says.

Amid all the technology upgrades, customer experience has been the key criterion. “We look to technology in everything we do in order to drive a good client experience,” Snelling explains. “On the back end, manual operations take away from the time you can spend interacting face-to-face with clients. Taking the friction out of back-office processes allows us to focus on the client that’s standing in front of us.”

Snelling adds that team members have responded favorably as they see how technology frees them to focus on their customers.

Santa Cruz County Bank will mark 20 years in business on Saturday, Feb. 3, and it remains one of the top ranked community banks in the country. It currently operates eight branches in Santa Cruz, Monterey and Santa Clara counties, with Salinas marking its newest branch. (It opened last year.) It’s those strong community ties that have been crucial to Santa Cruz County Bank’s success, said CEO Krista Snelling. Unlike a bigger operation, all deposits made at the bank are reinvested back into the three counties where it does business.

“If your deposits are with a major bank, who knows where that money is being deployed,” said Snelling. “We only lend here.” Community banks are financial institutions owned and operated locally, and serving a specific geographic area. They’re generally on the smaller side; the Federal Deposit Insurance Corporation (FDIC) loosely defines them as having less than $10 billion in assets. In other words, these aren’t your Bank of Americas or Wells Fargos of the world.

According to the latest stats available from the FDIC, the number of community banks nationally dropped from 6,802 to 4,750 between 2012 and 2019, though community banks acquired more than two-thirds of the community banks that closed during the study period. Count Santa Cruz County Bank among those; it merged with Lighthouse Bank in 2019. The bank currently employs around 150 people, five of whom have been with the company since Day 1, including executive vice president and chief marketing officer Mary Anne Carson, who was hired three months before the bank opened. The bank will honor Carson and four others at its anniversary celebration next month.

Last year was a turbulent one for smaller community banks. Rapidly rising interest rates caught some off-guard, leading to a run on deposits and the high-profile failure of several regional banks, including two in the San Francisco Bay Area. That spooked some customers, who moved their deposits to bigger banks and more lucrative savings and investment accounts, squeezing profits for small banks even further. Five regional banks failed in 2023, the most since 2017.

Santa Cruz County Bank wasn’t immune to these challenges. But the community bank, which celebrates its 20th anniversary on Saturday, Feb. 3, has weathered such storms before and did so again in 2023 by doubling down on what it sees as its strengths: its relationships with the local community.

“The No. 1 thing for us is that all of the decisions are made here in this market,” said CEO Krista Snelling. “Every decision that affects this market is made here by people who live and work here, and policies are set here. Our board of directors lives here. We know our market better than a bank where policies are set elsewhere.”

Started in 2004 by a group of business leaders who wanted a locally owned and operated bank, Santa Cruz County Bank now operates eight locations in three counties, holds $1.79 billion in assets and ranks as one of the region’s top Small Business Administration lenders.

When Santa Cruz County Bank merged with Lighthouse Bank, another Santa Cruz-based community bank, in 2019, not only did it add more locations but it also helped the bank expand its offerings and make technological investments. Along the way, the financial institution’s leadership has helped guide the bank through two recessions, a global pandemic and rising inflation — all while remaining locally owned and operated.

West Coast Community Bancorp ("Bancorp", OTCQX: SCZC), the parent company of Santa Cruz County Bank (the "Bank"), announced unaudited record earnings for the year ended December 31, 2023 of $35.2 million, a $4.2 million or 14% increase over 2022. Basic and diluted earnings per share in 2023 improved over 2022 by $0.55 and $0.54, respectively, to $4.18 and $4.16. Unaudited earnings for the quarter ended December 31, 2023 were $8.8 million, a decrease of 3% from $9.1 million in the prior quarter and a decrease of 12% from $10.0 million in the fourth quarter of 2022. Basic and diluted earnings per share in the fourth quarter of 2023 were both $1.05, and decreased over the prior quarter by $0.04 and $0.03, respectively. Both basic and diluted earnings per share in the fourth quarter of 2023 decreased over the prior year comparative quarter by $0.13.

President and CEO, Krista Snelling commented: "We are pleased to report record net income for the year and record gross loans at year-end. Our team grew loans despite the high interest rate environment, which speaks volumes for our relationship banking model and our reputation in the industry for responsiveness and delivery. In addition, we ranked as the top SBA lender by number of loans made in the Silicon Valley region for the SBA's 2023 fiscal year.

In February, we will celebrate our 20th anniversary as a community bank. The achievements of the past two decades are attributable to our dedicated employees, longstanding community partners, and loyal clients who value placing their deposits locally for the benefit of the communities we serve."

Santa Cruz County Bank tops other banks for number of small business loans issued locally

Santa Cruz County Bank issued 23 U.S. Small Business Administration (SBA) loans totaling $22.58 million to small businesses in greater Silicon Valley last year, making it the top such lender in the region.

SBA loans are backed by the federal agency, enabling financial institutions to provide business loans with more favorable terms than conventional loans. These are often a better option for small business owners who might not qualify for a traditional business loan, and the program helps encourage banks to lend to such companies.

Santa Cruz County Bank, which marks its 20th anniversary next month, continues to be one of the biggest local providers of SBA loans in the region, including Santa Clara, Santa Cruz and Monterey counties. Businesses receiving these loans include grocery stores, restaurants, gas stations and retail stores, among others.

“Our lending volume confirms our commitment to supporting small businesses to promote economic development and job growth,” said Susan Chandler, senior vice president and director of SBA lending.

Santa Cruz County Bank consummated a holding company reorganization with the formation of West Coast Community Bancorp, which went into effect on Aug. 18.

The formation of the bank’s holding company, West Coast Community Bancorp, was discussed in detail in the bank’s annual proxy statement, approved by shareholders on May 24, 2023, and subsequently approved by the bank’s regulators. As a result of the transaction, Santa Cruz County Bank has become a wholly-owned subsidiary of West Coast Community Bancorp, and shareholders of the bank have become shareholders of the holding company on a “one share for one share” basis. Shares of West Coast Community Bancorp began being quoted on the OTC Markets OTCQX U.S. Premier Market on Aug. 28 under the trading symbol SCZC, retaining continuity with the bank’s prior quotation and symbol.

The board of directors of West Coast Community Bancorp and Santa Cruz County Bank are identical, with Stephen D. Pahl serving as chairman, John C. Burroughs serving as vice chairman and corporate secretary. The board also includes Caroline D. Chapin, Kenneth R. Chappell, Craig French, Thomas N. Griffin, James L. Weisenstein and Krista Snelling, who is the president and CEO of the bank.

“We believe the formation of our holding company will provide additional flexibility for future capital needs necessary to respond to evolving changes in the banking and financial services industries and will allow us to take advantage of opportunities afforded by this restructure,” Snelling said. “There are no changes to the operations of Santa Cruz County Bank or its employees.”

Santa Cruz County Bank announced Shawn Lipman will succeed Susan Just as executive vice president and chief credit officer. Just has served in the chief credit officer role for the past two years and will leave the bank later this month.

In his 12-year career at Santa Cruz County Bank, Lipman has been promoted multiple times. He has served as senior vice president and director of credit administration for the last two years. Under his leadership, the bank’s credit portfolio has grown in size and complexity, with privately placed municipal bond purchases, loans issued under the New Market Tax Credit program, and structured credits originated by the bank’s asset-based lending division, which launched last year. In addition, Lipman led the department through systems conversions, the bank’s merger with Lighthouse Bank and the implementation of the Paycheck Protection Program.

Earlier in his career, Lipman served as senior vice president and regional portfolio manager at GMAC Commercial Finance, where he was responsible for managing new business for the western region. In addition, he served as senior relationship manager and team leader at Union Bank, managing a portfolio of loans throughout California.

“We are excited for Shawn to step into the role of chief credit officer. He has been a key employee of the bank for 12 years and has progressively advanced to a leadership position, making him the logical successor to the role of chief credit officer,” Krista Snelling, president and CEO of Santa Cruz County Bank, said. “His promotion is a natural next step in his career given his background, expertise and detailed knowledge of the bank’s clients and policies, and we are excited to work with Shawn as he takes the top credit role at the bank. Susan has been a valued member of the bank and our executive team for the past two years and we wish her well in her future endeavors.”

Around 50 men slipped into pairs of bright red and pink high heels Friday for a quick dash around the block in downtown Santa Cruz in the 2023 Santa Cruz County Bank Walk a Mile in Her Shoes event.

In its 11th year, the annual gathering originated as a fundraiser for Monarch Services and to promote awareness about domestic violence and sexual assault.

The Walk features male employees of Santa Cruz County Bank and their local business partners.

After a brief welcoming ceremony, the crowd of heeled runners burst out from the starting line in an awkward and jilted sprint.

“Let me tell you, even the first 50 feet was tough,” said Dug Fisher, senior vice president for County Bank. “But it’s worth it, to be able to help places like Monarch Services. They’re an amazing community service for our community.”

At the close of the race, Fischer was pulled from the cheering crowd to be presented the, “He’s Got Legs Award.”

Leeann Luna, Program Director of Monarch Services, said, “We are excited to partner, once again, in this fun event that supports our vital services to empower individuals, families and our communities to take action against violence and abuse.”

Monarch Services has been providing community assistance to survivors of violence for over 45 years. Their services include counseling, shelter, emergency financial aid, transportation, support groups and more. Monarch Services is the only rape crisis and human trafficking center in Santa Cruz County. All services are available in Spanish and English and are free or low cost.

Coming from a family of strawberry growers, Jaime Manriquez had been expected to eventually take over the family business.

But when his father brought home the family's first home computer, Manriquez's outlook quickly changed. The then-elementary school student went from future strawberry farmer to budding computer programmer.

It's perhaps fitting that as a professional, Manriquez has gone back to his roots, after a fashion. In the early stages of the Covid-19 outbreak, Manriquez, by then the chief information and chief information security officer at Santa Cruz County Bank, helped set up the technology needed to process the pandemic-related loans that allowed many local farmers to keep working.

Thanks to his and his team's efforts, which involved using artificial intelligence, the bank ended up processing $574 million worth of Paycheck Protection Program (PPP) loans, ultimately saving about 50,000 jobs.

"We set up an environment where we had three or four robots processing loans for those who needed PPP payouts," Manriquez said. "We automated that process."

A fourth-generation Mexican-American who grew up in Watsonville, Manriquez was well prepared for the effort. He'd been working in technical roles for nearly 25 years. As a technical-support engineer at International Business Machines Corp. around the turn of the millennium, he worked on a series of Y2K-related projects. He'd been with Santa Cruz County Bank, helping head its technology and information security operations, since before it opened in 2004.

Shelly Medina has played a critical role in the establishment and operation of successful asset-based lending businesses in Silicon Valley. Her most recent foray took place just last year, as she joined Santa Cruz County Bank to launch a new ABL division that serves emerging growth companies that require asset liquidity and flexible lines of credit.

To get the new division up and running, Medina employed her historical knowledge across nearly three decades in ABL to complete the many steps required to build internal workflows, including creating client application forms, legal agreements and loan documents, while identifying and implementing specialized software. Medina also coordinated and delivered internal employee training and communications for the new division.

As she has shown in building Santa Cruz County Bank’s ABL unit, Medina possesses unmatched skills that allow her to start from scratch and create operational and leading documentation teams within business units. Her management and leadership lead to quantifiable successes. She also has the proven ability to lead a startup operation through significant scale, having previously supported the launch of Bridge Bank’s factoring and ABL division in 2002.

Santa Cruz County Bank on Thursday announced the opening of a full-service branch in Salinas. The address of the bank's newest branch is 480 S. Main St., Salinas.

In January of 2021, Santa Cruz County Bank opened its first branch in Monterey County at 584 Munras Ave., in Monterey.

"We are excited for the opportunity to serve the Salinas Valley following our successful expansion into Monterey County in 2021," said Santa Cruz County Bank President and CEO, Krista Snelling in a prepared release.

Vic Davis' 43+ year career in community banking began at County Bank and Trust in Santa Cruz, where he served as Branch Operations Supervisor and Budget Manager. For ten years he was Chief Financial Officer of San Benito Bank in Hollister California. In his career, he also served as a senior level Auditor and Consultant for Bank Vision, Inc. He is a graduate of Pacific Coast Banking School in Washington and is an accredited ACH Professional and has held certifications as a professional in human resources and as a community bank internal auditor.

In his 14-year career at Santa Cruz County Bank, Mr. Davis has managed the bank's assets and liabilities, securities portfolio and Finance Department, all of which have grown in size 10-fold during his leadership. In addition, Mr. Davis led the department during the recession, through systems conversions and the merger with Lighthouse Bank and multiple, complex stock-related transactions.

Krista Snelling, President and CEO commented, "Vic has been a valued member of the bank and our executive team for over 14 years. Under his leadership, the bank has grown significantly and our accounting has also grown in complexity, which necessitates ongoing education, regulatory monitoring and evolving financial acumen. Vic's vast experience and auditing background have been instrumental to his role. He will be greatly missed by our entire team."

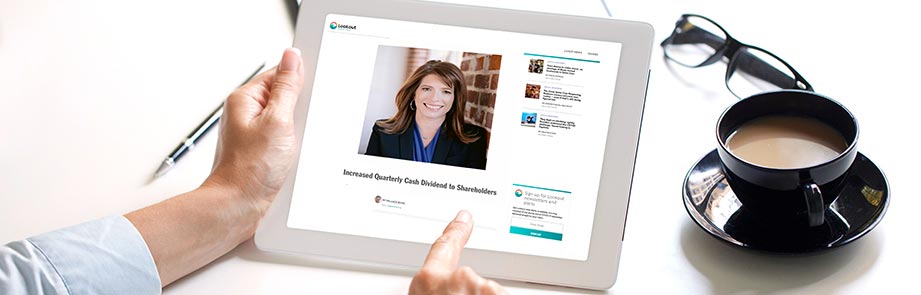

Santa Cruz County Bank www.sccountybank.com (OTCQX:SCZC), with assets over $1.76 billion, is a top-rated community bank headquartered in Santa Cruz County. On September 20, 2022, the Bank’s Board of Directors declared an increased quarterly cash dividend of $0.125 per share. The dividend is payable on October 11, 2022 to shareholders of record as of the close of business on October 4, 2022.

Chairman William J. Hansen stated, “We are pleased to continue to reward our shareholders for their investment in our stock. In 2022, the Board of Directors of Santa Cruz County Bank have declared a 2-for-1 stock split, two increased quarterly cash dividends, and a $5 million share repurchase program.”

For the quarter that ended June 30, 2022, Santa Cruz County Bank reported $6.37 million in net income, a 20% increase over the same period in 2021. Return on average equity was 13.77% for the quarter ended June 30, 2022. The book value per share of Santa Cruz County Bank's common stock at June 30, 2022 was $21.73, an increase of $0.75 from the same period in 2021. Shareholders' equity grew to $186 million, an $6.94 million increase compared to the same period in 2021.

Co-hosted by Santa Cruz County Bank and organized by Santa Cruz Works, everyone is invited to join the 5th Annual Blue Innovation outdoor event on September 11th.

Hosted at the incomparable Seymour Marine Discovery Center at UC Santa Cruz, this event will welcome over 3,000 attendees from September 11 - 13 to connect researchers, organizations and community members who are passionate about protecting our oceans and water sources.

“Talk about perfect fit! Blue Innovation and SCCB are a marriage of community engagement. SCCB is a generous leader in our community, assisting startups, researchers, and entrepreneurs who are building a better future for our families and the world.” — Doug Erickson, Executive Director of Santa Cruz Works

In our current day and age, there is an undisputed, urgent need to tackle challenges created by climate change. Blue Innovation provides an educational opportunity to uncover ways to improve ocean and water sustainability. Over 50 exhibitors will come together to exhibit their solutions ranging from ocean-safe alternatives to plastics, sea wall restoration, and transportation. Come out to enjoy food trucks, live music and exhibitors interactive exhibits.

Having a bank that knows who you are, understands your situation, and the best way to work with you is invaluable. Money is a sensitive matter for everyone, and consumers today want more than a place to keep their money safe — they want help solving financial problems.

For many Americans, that’s becoming more difficult to find. Community banks foster that type of trust with account holders because their employees live in the communities where they work, and community banks reinvest in the communities they serve. But community banks are closing — or being acquired — at an alarming rate.

The number of community banks has dropped significantly over the last two decades. In 2000, there were 8,300 community banks in the US. By the end of 2020, that number had been reduced to 4,277.

In the early 2000s, a group of local business owners in Santa Cruz County, California, decided to take action to open a bank in their community at a time when the last of the local banks had vanished due to a merger. A group of investors came together and raised capital to create Santa Cruz County Bank, which opened in 2004.

Today, the bank operates seven branches across California’s Bay Area and Central Coast, with another coming soon. The people the bank serves are all neighbors, friends, and community members. And Santa Cruz County Bank wants to ensure it stays that way.

What would you like to accomplish in the next 10 years? Grow the bank and provide opportunity to clients and my team.

What’s the best piece of advice you have ever received? Use your authenticity as your secret weapon.

What is the biggest challenge facing women who want to take on leadership roles — and what do you think you can do to change that? Lack of female mentors. I plan to be one for as many women as I can!

What is a moment in your career you are most proud of? Being appointed one of only 9% female bank CEOs in the Western United States.

Who has been your most supportive mentor and why? James Beckwith, CEO of Five Star Bank, because he told me I should be a CEO before I knew I should be a CEO.

Something about you that would surprise others? I used to be very quiet when I was in school. Unbelievable now!

Santa Cruz County Bank launched an asset-based lending division, which will be led by Lee Shodiss and Shelly Medina. The bank’s new asset-based lending division will specialize in serving business clients and emerging growth companies requiring asset liquidity and flexible lines of credit in addition to full banking services. The addition of an asset-based lending division showcases the bank’s commitment to supporting small business. The division is based at the bank’s Cupertino, CA office to serve clients in Silicon Valley, the Greater Bay Area and throughout California.

The bank’s asset-based lending division is directed by Shodiss, an industry veteran with 30 years of experience in asset-based and innovation markets serving Silicon Valley and technology centers throughout the country. Medina leads the asset-based lending division as operations manager.

“We experienced firsthand the pandemic’s profound impact on working capital needs of many businesses,” Krista Snelling, president and CEO of Santa Cruz County Bank, said. “Our new asset-based lending division complements the bank’s significant growth and ability to provide capital to businesses through specialty financing solutions. We see great opportunity, particularly in serving the high concentration of businesses centered in technology and innovation in Silicon Valley. The hiring of Lee and Shelly, both well-known experts in ABL, expands our team at the bank’s Cupertino branch and positions us advantageously to serve the market, grow our portfolio and support our existing client relationships.”

© 2024 Santa Cruz County Bank. All rights reserved.

California Consumer Privacy Act Notice | Privacy Policy | Member FDIC | ![]() Equal Housing Lender

Equal Housing Lender

Santa Cruz County Bank has no control over information at any site hyperlinked to or from this site. Santa Cruz County Bank makes no representation concerning and is not responsible for the quality, content, nature, or reliability of any hyperlinked site and is providing this hyperlink to you only as a convenience. The inclusion of any hyperlink does not imply any endorsement, investigation, verification or monitoring by Santa Cruz County Bank of any information in any hyperlinked site. In no event shall Santa Cruz County Bank be responsible for your use of a hyperlinked site.

Santa Cruz County Bank has no control over information at any site hyperlinked to or from this site. Santa Cruz County Bank makes no representation concerning and is not responsible for the quality, content, nature, or reliability of any hyperlinked site and is providing this hyperlink to you only as a convenience. The inclusion of any hyperlink does not imply any endorsement, investigation, verification or monitoring by Santa Cruz County Bank of any information in any hyperlinked site. In no event shall Santa Cruz County Bank be responsible for your use of a hyperlinked site.

Santa Cruz County Bank has no control over information at any site hyperlinked to or from this site. Santa Cruz County Bank makes no representation concerning and is not responsible for the quality, content, nature, or reliability of any hyperlinked site and is providing this hyperlink to you only as a convenience. The inclusion of any hyperlink does not imply any endorsement, investigation, verification or monitoring by Santa Cruz County Bank of any information in any hyperlinked site. In no event shall Santa Cruz County Bank be responsible for your use of a hyperlinked site.

Santa Cruz County Bank has no control over information at any site hyperlinked to or from this site. Santa Cruz County Bank makes no representation concerning and is not responsible for the quality, content, nature, or reliability of any hyperlinked site and is providing this hyperlink to you only as a convenience. The inclusion of any hyperlink does not imply any endorsement, investigation, verification or monitoring by Santa Cruz County Bank of any information in any hyperlinked site. In no event shall Santa Cruz County Bank be responsible for your use of a hyperlinked site.

Santa Cruz County Bank has no control over information at any site hyperlinked to or from this site. Santa Cruz County Bank makes no representation concerning and is not responsible for the quality, content, nature, or reliability of any hyperlinked site and is providing this hyperlink to you only as a convenience. The inclusion of any hyperlink does not imply any endorsement, investigation, verification or monitoring by Santa Cruz County Bank of any information in any hyperlinked site. In no event shall Santa Cruz County Bank be responsible for your use of a hyperlinked site.

Santa Cruz County Bank has no control over information at any site hyperlinked to or from this site. Santa Cruz County Bank makes no representation concerning and is not responsible for the quality, content, nature, or reliability of any hyperlinked site and is providing this hyperlink to you only as a convenience. The inclusion of any hyperlink does not imply any endorsement, investigation, verification or monitoring by Santa Cruz County Bank of any information in any hyperlinked site. In no event shall Santa Cruz County Bank be responsible for your use of a hyperlinked site.

Santa Cruz County Bank has no control over information at any site hyperlinked to or from this site. Santa Cruz County Bank makes no representation concerning and is not responsible for the quality, content, nature, or reliability of any hyperlinked site and is providing this hyperlink to you only as a convenience. The inclusion of any hyperlink does not imply any endorsement, investigation, verification or monitoring by Santa Cruz County Bank of any information in any hyperlinked site. In no event shall Santa Cruz County Bank be responsible for your use of a hyperlinked site.

Santa Cruz County Bank has no control over information at any site hyperlinked to or from this site. Santa Cruz County Bank makes no representation concerning and is not responsible for the quality, content, nature, or reliability of any hyperlinked site and is providing this hyperlink to you only as a convenience. The inclusion of any hyperlink does not imply any endorsement, investigation, verification or monitoring by Santa Cruz County Bank of any information in any hyperlinked site. In no event shall Santa Cruz County Bank be responsible for your use of a hyperlinked site.

Santa Cruz County Bank has no control over information at any site hyperlinked to or from this site. Santa Cruz County Bank makes no representation concerning and is not responsible for the quality, content, nature, or reliability of any hyperlinked site and is providing this hyperlink to you only as a convenience. The inclusion of any hyperlink does not imply any endorsement, investigation, verification or monitoring by Santa Cruz County Bank of any information in any hyperlinked site. In no event shall Santa Cruz County Bank be responsible for your use of a hyperlinked site.

Santa Cruz County Bank has no control over information at any site hyperlinked to or from this site. Santa Cruz County Bank makes no representation concerning and is not responsible for the quality, content, nature, or reliability of any hyperlinked site and is providing this hyperlink to you only as a convenience. The inclusion of any hyperlink does not imply any endorsement, investigation, verification or monitoring by Santa Cruz County Bank of any information in any hyperlinked site. In no event shall Santa Cruz County Bank be responsible for your use of a hyperlinked site.

Santa Cruz County Bank has no control over information at any site hyperlinked to or from this site. Santa Cruz County Bank makes no representation concerning and is not responsible for the quality, content, nature, or reliability of any hyperlinked site and is providing this hyperlink to you only as a convenience. The inclusion of any hyperlink does not imply any endorsement, investigation, verification or monitoring by Santa Cruz County Bank of any information in any hyperlinked site. In no event shall Santa Cruz County Bank be responsible for your use of a hyperlinked site.

Santa Cruz County Bank has no control over information at any site hyperlinked to or from this site. Santa Cruz County Bank makes no representation concerning and is not responsible for the quality, content, nature, or reliability of any hyperlinked site and is providing this hyperlink to you only as a convenience. The inclusion of any hyperlink does not imply any endorsement, investigation, verification or monitoring by Santa Cruz County Bank of any information in any hyperlinked site. In no event shall Santa Cruz County Bank be responsible for your use of a hyperlinked site.

Santa Cruz County Bank has no control over information at any site hyperlinked to or from this site. Santa Cruz County Bank makes no representation concerning and is not responsible for the quality, content, nature, or reliability of any hyperlinked site and is providing this hyperlink to you only as a convenience. The inclusion of any hyperlink does not imply any endorsement, investigation, verification or monitoring by Santa Cruz County Bank of any information in any hyperlinked site. In no event shall Santa Cruz County Bank be responsible for your use of a hyperlinked site.

Santa Cruz County Bank has no control over information at any site hyperlinked to or from this site. Santa Cruz County Bank makes no representation concerning and is not responsible for the quality, content, nature, or reliability of any hyperlinked site and is providing this hyperlink to you only as a convenience. The inclusion of any hyperlink does not imply any endorsement, investigation, verification or monitoring by Santa Cruz County Bank of any information in any hyperlinked site. In no event shall Santa Cruz County Bank be responsible for your use of a hyperlinked site.

Santa Cruz County Bank has no control over information at any site hyperlinked to or from this site. Santa Cruz County Bank makes no representation concerning and is not responsible for the quality, content, nature, or reliability of any hyperlinked site and is providing this hyperlink to you only as a convenience. The inclusion of any hyperlink does not imply any endorsement, investigation, verification or monitoring by Santa Cruz County Bank of any information in any hyperlinked site. In no event shall Santa Cruz County Bank be responsible for your use of a hyperlinked site.

Santa Cruz County Bank has no control over information at any site hyperlinked to or from this site. Santa Cruz County Bank makes no representation concerning and is not responsible for the quality, content, nature, or reliability of any hyperlinked site and is providing this hyperlink to you only as a convenience. The inclusion of any hyperlink does not imply any endorsement, investigation, verification or monitoring by Santa Cruz County Bank of any information in any hyperlinked site. In no event shall Santa Cruz County Bank be responsible for your use of a hyperlinked site.

Santa Cruz County Bank has no control over information at any site hyperlinked to or from this site. Santa Cruz County Bank makes no representation concerning and is not responsible for the quality, content, nature, or reliability of any hyperlinked site and is providing this hyperlink to you only as a convenience. The inclusion of any hyperlink does not imply any endorsement, investigation, verification or monitoring by Santa Cruz County Bank of any information in any hyperlinked site. In no event shall Santa Cruz County Bank be responsible for your use of a hyperlinked site.

Santa Cruz County Bank has no control over information at any site hyperlinked to or from this site. Santa Cruz County Bank makes no representation concerning and is not responsible for the quality, content, nature, or reliability of any hyperlinked site and is providing this hyperlink to you only as a convenience. The inclusion of any hyperlink does not imply any endorsement, investigation, verification or monitoring by Santa Cruz County Bank of any information in any hyperlinked site. In no event shall Santa Cruz County Bank be responsible for your use of a hyperlinked site.

Santa Cruz County Bank has no control over information at any site hyperlinked to or from this site. Santa Cruz County Bank makes no representation concerning and is not responsible for the quality, content, nature, or reliability of any hyperlinked site and is providing this hyperlink to you only as a convenience. The inclusion of any hyperlink does not imply any endorsement, investigation, verification or monitoring by Santa Cruz County Bank of any information in any hyperlinked site. In no event shall Santa Cruz County Bank be responsible for your use of a hyperlinked site.

Santa Cruz County Bank has no control over information at any site hyperlinked to or from this site. Santa Cruz County Bank makes no representation concerning and is not responsible for the quality, content, nature, or reliability of any hyperlinked site and is providing this hyperlink to you only as a convenience. The inclusion of any hyperlink does not imply any endorsement, investigation, verification or monitoring by Santa Cruz County Bank of any information in any hyperlinked site. In no event shall Santa Cruz County Bank be responsible for your use of a hyperlinked site.

Santa Cruz County Bank has no control over information at any site hyperlinked to or from this site. Santa Cruz County Bank makes no representation concerning and is not responsible for the quality, content, nature, or reliability of any hyperlinked site and is providing this hyperlink to you only as a convenience. The inclusion of any hyperlink does not imply any endorsement, investigation, verification or monitoring by Santa Cruz County Bank of any information in any hyperlinked site. In no event shall Santa Cruz County Bank be responsible for your use of a hyperlinked site.